INTRODUCTION

INTRODUCTION

A board of trustees has the fiduciary duty to invest in the best interest of a pension fund’s beneficiaries: the participants and the retirees. This is known as the prudent person rule. Trustees’ characteristics should therefore not influence their decision making. Yet, many trustees are middle-aged men. It is not unlikely that these two characteristics influence the investment decisions that trustees make on behalf of beneficiaries. In this article, we empirically examine whether the age and gender of trustees influence the strategic equity allocation. We focus on the strategic equity allocation because this is the key variable in many life-cycle models and is a key component in any pension fund’s portfolio. As a robustness check, we also analyze the impact of age and gender on the total strategic allocation to equity, private equity, hedge funds and commodities. If trustees’ characteristics such as age and gender influence investment decisions, they might select a strategic asset allocation that does not fully reflect the preferences and characteristics of beneficiaries. This would be at odds with the prudent person rule of investments that is at the heart of pension fund governance.

THE INSTITUTIONAL SETTING AND PENSION FUND GOVERNANCE

The Dutch occupational system is an ideal laboratory to study the relation between investment decisions and board characteristics. The assets under management of the Dutch occupational pension funds is almost twice the GDP of the Netherlands. A pension fund in the Netherlands is set up as a trust at arm’s length of the sponsor. The goal of a pension fund is to execute the pension contract that employers and workers agree upon. Trustees are responsible for managing the pension fund’s assets and administrating beneficiaries’ benefits, within the limits of laws and regulations. In doing so, trustees are monitored by means of internal and external supervision. A supervisory board, a visitation committee or non-executive trustees are responsible for internal supervision. External supervision is in the hand of two independent supervisory authorities. The Dutch Central Bank (“De Nederlandsche Bank”, DNB) exercises prudential supervision and the Authority for the Financial Markets (AFM) is responsible for market conduct supervision.

ONE OF THE KEY PILLARS IN SUPERVISION IS THE PRUDENT PERSON RULE

One of the key pillars in supervision is the prudent person rule. This rule is formalized in Article 135 of the Dutch Pension Act. It is a, so-called, open norm and does not contain quantitative investment restrictions. Nonetheless, the Pension Act does specify the prudent person rule in a qualitative way. The board of trustees needs to verify the risk aversion level of beneficiaries and the investment policy must be in line with the structure and duration of pension benefits. The retirement savings must be invested in such a way as to guarantee the security, quality, liquidity and return of the portfolio as a whole. Further, the prudent person rule requires a pension fund to diversify its investments, and the larger part of the assets should be invested in regulated markets. Finally, the board of trustees needs to disclose its stance with respect to sustainable investing.

The prudent person rule implies that trustees need to invest in the best interests of the beneficiaries. This rule is key because a pension plan is one of the most important financial products for employees. Employees automatically enroll in the pension plan offered by the employer. There are huge barriers for employees to exit from a pension plan because they would need to resign from their job to be able to transfer accrued pension benefits. Furthermore, retirees have no possibility to exit the pension fund at all. For employers, a pension plan is important to compete in the labor market. For these reasons, employees, retirees and employers are represented in a pension fund’s board of trustees. A fair representation of stakeholders’ interests is central to good pension fund governance. However, the Pension Act does not contain requirements concerning age or gender representation. Nonetheless, board diversity has been an object of discussion within the pension fund sector itself for many years. In 2014, this discussion led to the introduction of the ‘Code of Dutch Pension Funds’ as an instrument of self regulation. The code does have a guideline on age: the board will comprise at least one member under the age of 40 and one over the age of 40. It also has a guideline on gender and states that at least one woman and one man hold a seat in the board of trustees. Pension funds follow the code under the comply-or explain principle. This means that they comply with the code or explain and justify in their annual report why they deviate from it (Pensioenfederatie, 2017). The fact that the pension sector issued guidelines on age and gender implies that these are considered important to good governance.

PENSION FUND INVESTMENT POLICY

PENSION FUND INVESTMENT POLICY

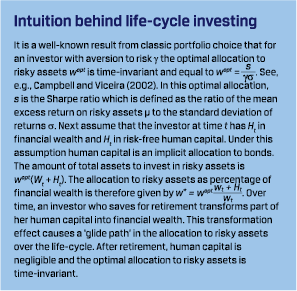

Before we can test if age and gender of trustees influence strategic equity allocation decisions, we need to have a benchmark model that describes a pension fund’s investment policy. Based on the well-established life-cycle literature, we expect pension funds to follow a life-cycle investment strategy, see, e.g., Bodie, Merton and Samuelson (1992), Campbell and Viceira (2002), and Cocco, Gomes and Maenhout (2005). Key to the optimal investment strategy over the life cycle is the role of human capital. Young workers are endowed with a high human capital, or a high present value of future labor income. If the return on their human capital is weakly correlated with the return on the equity market, the young have a large implicit position in risk-free bonds and hence prefer to hold a significant fraction of their financial wealth in risky assets. This argument reverses for middle-aged workers because their human capital is lower. If we apply this to a pension fund setting, we expect that the strategic equity allocation is negatively related to the average age of active participants. This implies that the strategic equity allocation is expected to go down for a higher average age of active participants. Note that the age of active participants is a proxy for human capital. The box provides some further intuition behind life-cycle investing.

In addition to the average age of active participants, we expect pension fund size, funding ratio, interest rate hedging and pension fund type to impact a pension fund’s investment policy. Size matters because large pension funds profit from economies of scale, see Broeders, van Oord and Rijsbergen (2016). The relation between funding ratio and equity allocation can be twofold. On the one hand, pension funds may decide to diminish investment risks and hence reduce their equity allocation in case the funding ratio is low. On the other hand, pension funds may decide to rebalance their portfolio back to strategic weights, also if this means that the actual allocation to equity and other risky asset classes needs to be increased. Dutch pension fund legislation allows such a rebalancing policy also in case of underfunding. Interest rate hedging potentially also influences investment policy although the impact is again not straightforward. By hedging interest rate risk with interest rate swaps, a pension fund can take more risks elsewhere, e.g., by investing more in risky asset classes. Interest rate risk hedging however also requires a pension fund to have sufficient cash and short-term bonds available for collateral requirements, see Broeders, Jansen and Werker (2020). We also control for pension fund type. Institutional differences between industrywide pension funds, corporate pension funds and professional group pension funds might influence strategic investment decisions. Especially in the context of corporate pension plans there are many papers on how regulation and management compensation incentives influence investment policies, see, e.g., Rauh (2009) and Anantharaman and Lee (2014).

DATA AND SUMMARY STATISTICS

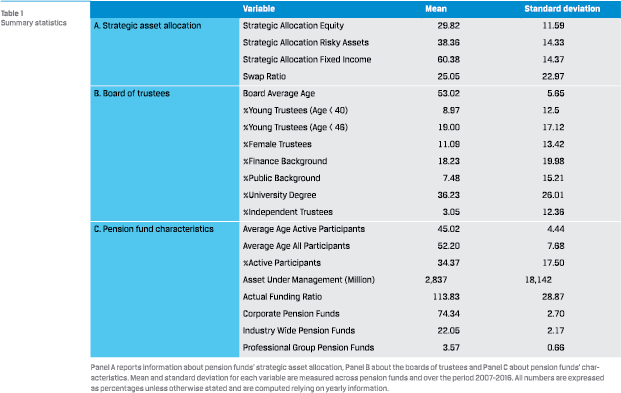

In our empirical analysis, we use an unbalanced panel of 437 occupational pension funds that essentially reflect the entire population of defined benefit pension funds in the Netherlands over the period 2007 through 2016. The data are free from reporting biases. All pension are obliged to report key financial information such as the strategic asset allocation, total assets under management and funding ratio on a yearly basis to DNB. We use the marked-to-market funding ratio and not the 12-months smoothed policy funding ratio that was introduced in 2015. The marked-to-market funding ratio is a better indicator of the current financial position. Information on the board of trustees is also reported on a yearly basis and contains name, age, gender and tenure of each individual trustee. Our database also includes the stakeholder group that each trustee represents. A trustee can represent the participants (current or former employees), the retirees or the employer. In addition, a trustee can also be appointed because of his or her expertise, without representing a specific stakeholder group. Such a person is referred to as an independent trustee. Moreover, to enrich our database we additionally collect information about previous employments and education of individual trustees through the social media website LinkedIn.com. A trustee has a financial background if he or she has worked in fields such as finance, accounting or at an economics related institution. A trustee has a public background if he or she has worked for government institutions, municipalities, labor unions, in healthcare or other social institutions. We also track if a trustee has indicated on LinkedIn.com to have a university degree.

Table 1 contains the averages and standard deviations of the main variables in our analysis across pension funds and time. On average, pension funds allocate 30 percent of their portfolio to equity, 60 percent to fixed income and the remainder of 10 percent is distributed among real estate, private equity, hedge funds and commodities. These allocations have been relatively stable over the sample period. The average swap ratio is 25 percent. This means that pension funds on average hedge a quarter of the interest rate risk mismatch between assets and liabilities using interest rates swaps. Pension funds also use longterm bonds to hedge interest rate risk.

Table 1 contains the averages and standard deviations of the main variables in our analysis across pension funds and time. On average, pension funds allocate 30 percent of their portfolio to equity, 60 percent to fixed income and the remainder of 10 percent is distributed among real estate, private equity, hedge funds and commodities. These allocations have been relatively stable over the sample period. The average swap ratio is 25 percent. This means that pension funds on average hedge a quarter of the interest rate risk mismatch between assets and liabilities using interest rates swaps. Pension funds also use longterm bonds to hedge interest rate risk.

THE AVERAGE BOARD MEMBER IS A 54 YEAR MALE

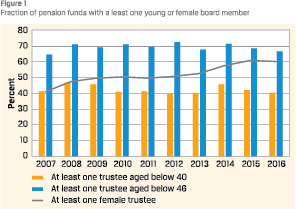

The average age of a pension fund board member is 54 year. The fraction of board members younger than 40 year is only nine percent. This fraction is fairly stable over the sample period. An age of 40 year is the threshold of a young trustee in the Code of Dutch Pension Funds. Considering that the average board size is seven members, less than one out of seven trustees is on average young. The fraction of board members younger than 46 year, or the 25th percentile of the age distribution of trustees, is 19 percent. The average fraction of female trustees is 11 percent. This fraction grows from eight percent at the beginning to 15 percent at the end of the sample period. These statistics provide evidence that both the young and female population are underrepresented in boards of trustees. Figure 1 shows the fraction of pension funds with at least one trustee younger than 40, at least one trustee younger than 46 and with at least one female in the board. Over time, only 42 percent of the pension funds have at least one trustee younger than 40 in their board and 69 percent of the pension funds have at least one trustee younger than 46 in their board. Both fractions are fairly stable over time. The fraction of pension funds with at least one female in the board increases over time from 41 percent in 2007 to 60 percent in 2016. Yet, in 2016 on average only 15 percent of trustees is female, which is far from a proportionate representation because women count for 46 percent of the employed labor force in the Netherlands, according to Statistics Netherlands. Some 18 percent of board members have a financial background, seven percent have a public background and 36 percent have a university degree. Only three percent of trustees are independent.

YOUNG AND FEMALES ARE UNDERREPRESENTED IN THE BOARDS OF TRUSTEES

Our primary control variable is the average age of active participants. Across all pension funds the average age of active participants is 45.0 year (the median age is 44.7 year). We use the average age of active participants because it influences the strategic equity allocation more strongly than the average age of all participants. The reason is that retirees no longer possess human capital, so for retirees the theoretical life-cycle is a fixed asset allocation, see Bikker, Broeders, Hollanders and Ponds (2012). Note that the average age of active participants is significantly lower compared to the average age of trustees. Even the average age of all beneficiaries, including retirees, of 52 year is below the average age of trustees. The other control variables are pension fund size to correct for a potential size effect, funding ratio, swap ratio and pension fund type. The average total assets under management is close to three billion euro, even though this number is affected by a small number of large pension funds. Pension funds display an average funding ratio of 114 percent in the sample period. The distribution across pension fund type reads as follows: 74 percent are corporate pension funds, 22 percent are industry-wide pension funds and 4 percent are professional group pension funds.

Our primary control variable is the average age of active participants. Across all pension funds the average age of active participants is 45.0 year (the median age is 44.7 year). We use the average age of active participants because it influences the strategic equity allocation more strongly than the average age of all participants. The reason is that retirees no longer possess human capital, so for retirees the theoretical life-cycle is a fixed asset allocation, see Bikker, Broeders, Hollanders and Ponds (2012). Note that the average age of active participants is significantly lower compared to the average age of trustees. Even the average age of all beneficiaries, including retirees, of 52 year is below the average age of trustees. The other control variables are pension fund size to correct for a potential size effect, funding ratio, swap ratio and pension fund type. The average total assets under management is close to three billion euro, even though this number is affected by a small number of large pension funds. Pension funds display an average funding ratio of 114 percent in the sample period. The distribution across pension fund type reads as follows: 74 percent are corporate pension funds, 22 percent are industry-wide pension funds and 4 percent are professional group pension funds.

RESULTS

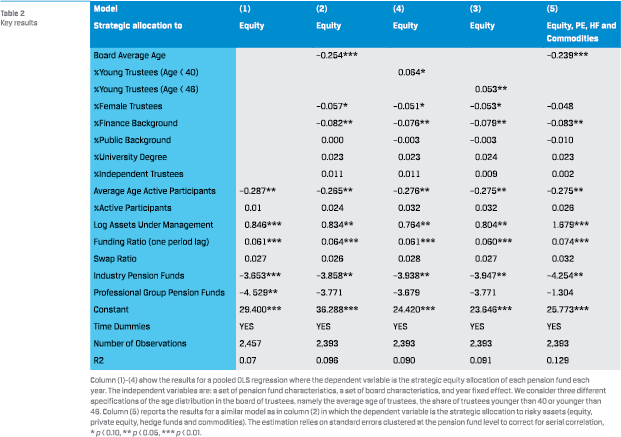

We test the impact of the age and gender of trustees on the strategic equity allocation using pooled OLS regressions with standard errors clustered at the pension fund level. This approach is robust for the fact that the number of pension funds in our sample decreases over time due to a consolidation trend. We use year dummies in the regression to control for changes in economic and regulatory conditions that might influence investment decisions in a given year, such as a change in the discount rates following the introduction of the Ultimate Forward Rate in 2012. For more details on the econometrics of our approach see Bauer et al. (2020). Before we go into our key results, we first run a baseline model in Table 2, column (1) without any of the trustee characteristics. We see that the average age of active participants has a statistically significant and negative impact on the strategic equity allocation. This result is consistent with life-cycle theory. If the average age increases by one year, the strategic equity allocation decreases by almost 0.30 percentage points.

If we add trustee characteristics to our baseline model, we observe two phenomena in the data: an age-effect and a gendereffect. First, we report a statistically significant age-effect in Table 2, column 2. Pension funds with more middle-aged trustees allocate less to equity compared to pension funds with young trustees in the board. If we multiply the regression coefficient of –0.254 from column (2) with the standard deviation of the average age of the board of 5.65 from Table 1, we find that for a one standard deviation increase in the board’s average age, the strategic allocation to equities decreases by 1.44 percentage points. If we run the same regression using the median board age, we find similar results that we do not report for reasons of brevity. In contrast, we find that a high fraction of young trustees in the board has a positive impact on the strategic equity allocation. Column (3) displays the impact of the fraction of trustees younger than 40. This fraction has a positive impact on the strategic equity allocation but only at the 10 percent significance level because of the low number of pension funds with trustees under the age of 40 year. Column (4) displays the impact of the fraction of trustees younger than 46 year on the strategic allocation. The regression coefficient of 0.053 has the following economic interpretation. Pension funds have an average board size of seven members. If one trustee out of seven is younger than 46 year this corresponds to 14 percent of the board members in an average board. Therefore, these pension funds allocate (14 x 0.053 =) 0.74 percentage points more to equity. As a robustness check, we do the analysis for the total strategic allocation to equity, private equity, hedge funds and commodities. The results in Table 2, column 5 show that the age-effect is again present and with a magnitude that is comparable to the strategic allocation to equity alone.

If we add trustee characteristics to our baseline model, we observe two phenomena in the data: an age-effect and a gendereffect. First, we report a statistically significant age-effect in Table 2, column 2. Pension funds with more middle-aged trustees allocate less to equity compared to pension funds with young trustees in the board. If we multiply the regression coefficient of –0.254 from column (2) with the standard deviation of the average age of the board of 5.65 from Table 1, we find that for a one standard deviation increase in the board’s average age, the strategic allocation to equities decreases by 1.44 percentage points. If we run the same regression using the median board age, we find similar results that we do not report for reasons of brevity. In contrast, we find that a high fraction of young trustees in the board has a positive impact on the strategic equity allocation. Column (3) displays the impact of the fraction of trustees younger than 40. This fraction has a positive impact on the strategic equity allocation but only at the 10 percent significance level because of the low number of pension funds with trustees under the age of 40 year. Column (4) displays the impact of the fraction of trustees younger than 46 year on the strategic allocation. The regression coefficient of 0.053 has the following economic interpretation. Pension funds have an average board size of seven members. If one trustee out of seven is younger than 46 year this corresponds to 14 percent of the board members in an average board. Therefore, these pension funds allocate (14 x 0.053 =) 0.74 percentage points more to equity. As a robustness check, we do the analysis for the total strategic allocation to equity, private equity, hedge funds and commodities. The results in Table 2, column 5 show that the age-effect is again present and with a magnitude that is comparable to the strategic allocation to equity alone.

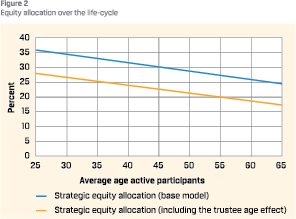

Figure 2 contains a graphical representation of the strategic equity allocation over the life cycle where the average age of active participants is our key variable of interest. The top line follows from the base model (Table 2, column 1) and bottom line from the model specification containing trustees’ characteristics (Table 2, column 2). Both lines show that the strategic equity allocation goes down if the average age of active participants increases. The location of the two lines relative to each other visualizes the impact of the age-effect. There is a structural, almost parallel, shift downward in the equity allocation over the life cycle when we include the average age of trustees. This is caused by the fact that the average board is much older than the average active participants (about nine years). This creates a misalignment between trustees and participants’ characteristics and means that the age effect of trustees leads to an investment policy that is more conservative compared to the one based on the average age of the active participants.

Figure 2 contains a graphical representation of the strategic equity allocation over the life cycle where the average age of active participants is our key variable of interest. The top line follows from the base model (Table 2, column 1) and bottom line from the model specification containing trustees’ characteristics (Table 2, column 2). Both lines show that the strategic equity allocation goes down if the average age of active participants increases. The location of the two lines relative to each other visualizes the impact of the age-effect. There is a structural, almost parallel, shift downward in the equity allocation over the life cycle when we include the average age of trustees. This is caused by the fact that the average board is much older than the average active participants (about nine years). This creates a misalignment between trustees and participants’ characteristics and means that the age effect of trustees leads to an investment policy that is more conservative compared to the one based on the average age of the active participants.

Second, we report evidence of a gender effect. In most model specifications, we find that pension funds with a higher share of female trustees allocate less to equity. However, the evidence of a gender effect is not conclusive, as the regression coefficients are only significant at the 10 percent level and the effect disappears if we assess the total strategic allocation to equity, private equity, hedge funds and commodities. However, when interpreting these results, we must take note of the fact that boards on average have less than one female member and many pension funds have no female trustees at all. Therefore, the existence of a gender effect indicates that female trustees are not a silent minority.

Moreover, we find that the share of trustees with a financial background is negatively related to the strategic equity allocation. This indicates that trustees with more financial expertise prefer to invest more in fixed income in order to hedge liabilities. Having a public background or a university degree as a trustee does not impact investment policy decisions. The fraction of independent trustees does not influence the strategic equity allocation either.

PENSION FUNDS WITH MORE YOUNG TRUSTEES ALLOCATE MORE TO EQUITY

The age and gender effects exist after controlling for key pension fund characteristics. This makes our results particularly strong. In line with life-cycle theories, we already mentioned that the strategic equity allocation is negatively related to the average age of active participants. The percentage of active participants has no statistically significant impact on the strategic equity allocation. This can be explained by the fact that the average age of active participants is more informative about the population. If the average age of active participants is low it is very likely that the fraction of active participants is high. We do find that large pension funds have a higher strategic equity allocation, following our economies of scale argument. However, the swap ratio has no statistically significant impact on the strategic equity allocation. This can be explained by the fact that interest rate risk hedging lowers the risk profile of a pension fund but also increases the allocation to cash and short-term bonds for collateral purposes. Further, the funding ratio is positively related to the strategic equity allocation. This indicates that pension funds with a higher funding ratio take more investment risk, and vice versa. Finally, we find that industry-wide pension funds and professional group pension funds invest less in equities compared to the control group of corporate pension funds. Corporate pension funds might be incentivized to take more investment risk because this increases the value of the claim that the corporation has on the pension fund’s surplus, see, e.g., Rauh (2009).

POTENTIAL EXPLANATIONS

Both the age and gender of trustees should not play a role in pension funds’ investment decisions. What could explain our findings to the contrary? We offer the following potential explanations. First, the willingness to take risk decreases with age, see, e.g., Dohmen, Falk, Golsteyn, Huffman and Sunde (2017). Empirical evidence indeed shows that individuals invest less in risky assets when they are older, see, e.g., Calvet, Campbell and Sodini (2007). Therefore, from an individual perspective, middle-aged trustees might prefer a lower equity allocation compared to relatively young trustees. Second, men are more overconfident and less risk averse compared to women. The empirical evidence for this can be found in, e.g., Barber and Odean (2001) and Vieider et al. (2015). Therefore, female trustees might prefer a lower equity allocation compared to male trustees. Following these two possible explanations, trustees might unknowingly project their own investment beliefs onto beneficiaries and, as a result, take biased decisions. This is known as the interpersonal empathy-gap in the socialpsychology literature, see Loewenstein (2005). Despite the underlying motivation, by valuing their own preferences trustees design strategic asset allocations that do not reflect the average characteristics and preferences of all beneficiaries.

CONCLUSION

We use a unique database on the strategic asset allocation and the board of trustees of Dutch pension funds to study if trustees’ characteristics influence investment decisions. Trustees have the fiduciary duty to invest pension fund assets in the best interests of the plan’s beneficiaries. Therefore, their own characteristics should not affect their decision making. Our results suggest that trustee characteristics do matter in practice. We find that pension funds with a higher average age of board members or with more female trustees, strategically allocate less to equity. This might lead to strategic asset allocations that do not reflect the preferences of pension plan beneficiaries. The age and gender effects show that a balanced representation of beneficiaries and board diversity are important to better align the investment policy with the characteristics and preferences of beneficiaries.

References

- Anantharaman, D. and Y.G. Lee (2014), Managerial risk taking incentives and corporate pension policy, Journal of Financial Economics, 111(2): 328351.

- Barber, B. and T. Odean (2001), Boys will be boys: Gender, overconfidence, and common stock investment, The Quarterly Journal of Economics 116(1): 261292.

- Bauer, R., R. Bogman, M. Bonetti and D. Broeders (2020), The impact of trustees’ age and representation on strategic asset allocations, working paper forthcoming on SSRN.

- Bikker, J, D.W.G.A. Broeders, D. Hollanders and E. Ponds (2012), Pension funds’ asset allocation and participant age: A test of the life-cycle model, Journal of Risk and Insurance 79(3): 595618.

- Bodie, Z., R.C., Merton and W.F. Samuelson (1992), Labor supply flexibility and portfolio choice in a life cycle model, Journal of Economic Dynamics and Control, 16(34): 427449.

- Broeders, D.W.G.A., A. van Oord and D.R. Rijsbergen (2016), Scale economies in pension fund investments: A dissection of investment costs across asset classes, Journal of International Money and Finance, 67, 147–171

- Broeders, D.W.G.A., K.A.E. Jansen and B.J.M. Werker (2020), Pension fund’s illiquid assets allocation under liquidity and capital requirements, Journal of Pension Economics and Finance, forthcoming.

- Calvet, L.E., J.Y. Campbell and P. Sodini (2007), Down or out: Assessing the welfare costs of household investment mistakes, Journal of Political Economy, 115(5): 707747.

- Campbell, J.Y. and L.M. Viceira (2002), Strategic asset allocation: Portfolio choice for long-term investors, Clarendon Lectures in Economic.

- Cocco, J.F., F.J. Gomes P.J. and Maenhout (2005), Consumption and portfolio choice over the life cycle, Review of Financial Studies, 18(2): 491533.

- Dohmen, T., A. Falk, B.H.H. Golsteyn, D. Huffman and U. Sunde (2017), Risk attitudes across the life course, Economic Journal, 127(605): 95116.

- Loewenstein, G. (2005), Hot-cold empathy gaps and medical decision making, Health Psychology, 24(4S): S49-S56.

- Pensioenfederatie (2017), Code of Dutch Pension Funds, www.pensioenfederatie.nl/stream/ codeofthedutchpensionfundsenglish2017.pdf.

- Rauh, J.D. (2009), Risk shifting versus risk management: Investment policy in corporate pension plans. Review of Financial Studies, 22(7): 26872733.

- Vieider, F.M., M. Lefebvre, R. Bouchouicha, T. Chmura, R. Hakimov, M. Krawczyk and P. Martinsson (2015), Common components of risk and uncertainty attitudes across contexts and domains: Evidence from 30 countries, Journal of the European Economic Association, 13(3): 421452.

Note

- This article is written in a personal capacity and does not necessarily reflect the opinion of DNB or KPMG.

in VBA Journaal door Rob Bauer, Rien Bogman, Matteo Bonetti and Dirk Broeders